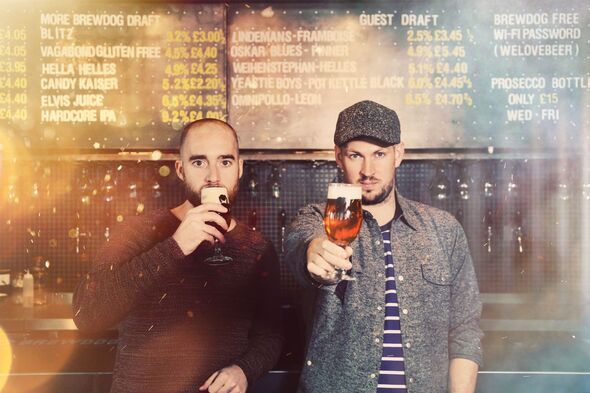

Hundreds of Brewdog workers were sacked yesterday in one of the most brutal mass redundancies in hospitality history after US cannabis-to-beverage giant Tilray Brands snapped up the troubled Scottish brewer's UK operations, brand and 11 pubs for just £33 million. The deal, completed on Monday after Brewdog collapsed into administration, saved 733 jobs by transferring them to Tilray. But 38 bars across the UK were shut immediately, axing 484 positions with no warning.

Unite union organiser Bryan Simpson called the process "morally repugnant". Staff received 25 minutes' notice of a 15-minute Zoom call on which cameras were switched off and questions were banned. Bryan Simpson said: "I've been representing bar workers for over a decade and this is the worst mass redundancy I have dealt with, including during the pandemic."

Many workers learned they would not be paid for weekend shifts or February overtime. Accrued holiday pay was wiped out. They were told to claim statutory redundancy and unpaid wages from the Government's Insolvency Service - at taxpayers' expense.

One sacked employee told the BBC: "They've washed their hands of us. We can't even collect our belongings without going through the administrators. And we've been warned not to speak out."

Tilray, listed in New York and Toronto, bought the global Brewdog brand, intellectual property, UK brewing operations and 11 profitable brewpubs, including Edinburgh, Manchester, Birmingham, Dublin and Canary Wharf. The assets generate roughly $200 million (£154 million) in annual revenue and $6-8 million in adjusted EBITDA, with Tilray forecasting cash-flow positivity from 2027.

Chairman and chief executive Irwin Simon hailed the purchase as a chance to "refocus Brewdog on the craft beer excellence that made it beloved". Irwin Simon promised investment to restore growth and said the combined Tilray beverage platform would hit $500 million in annual revenue.

Yet for thousands of small investors in Brewdog's Equity for Punks scheme - launched in 2009 and once touted as a way for fans to own a slice of the punk empire - there is nothing. The 200,000 backers, many ordinary drinkers who sank £500 or more into shares, will receive zero return. Preference shares held by US private-equity firm TSG Consumer Partners since 2017 take priority.

Investor Richard Fisher, who lost £12,000, said: "It's being sold for parts. There was never going to be anything left for us."

Administrators AlixPartners confirmed equity holders, including staff shareholders, would get "pennies on the pound or probably nothing".

The collapse marks a grim end for the company founded in 2007 by James Watt and Martin Dickie, once valued at more than £2 billion. Years of scandals over workplace culture, allegations of bullying and inappropriate behaviour, the abandonment of the living wage and earlier bar closures had already shredded its reputation.

Mr Watt stepped down as CEO in 2024; Mr Dickie left in 2025. Last month the firm was put up for sale. Now the "punk" beer empire has been carved up, its bars shuttered and its workers discarded while a new owner promises to revive the brand.

Brewdog has been approached for comment.