If you are planning to buy your dream home, your Provident Fund (PF) savings could play a crucial role. With the latest updates under Employees' Provident Fund Organisation (EPFO) 3.0, the process of withdrawing PF money has become faster, more digital, and user-friendly. However, before using your retirement savings for a home purchase, it’s important to understand the rules, eligibility, and potential risks involved.

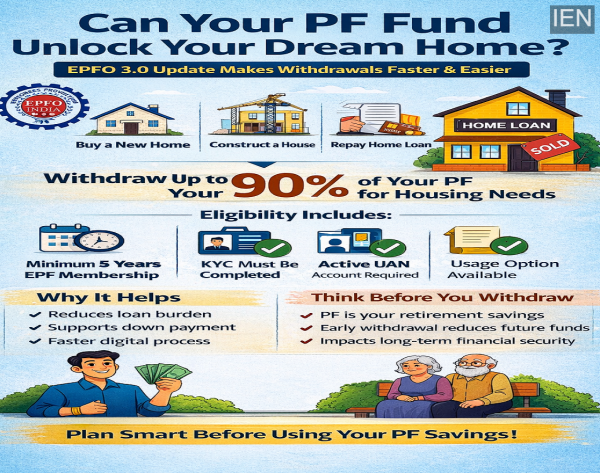

Yes, EPFO allows members to withdraw a significant portion of their PF balance for housing purposes. Under existing rules, eligible employees can withdraw up to 90% of their PF corpus for:

Buying a ready property

Constructing a house

Repaying a home loan

This provision can provide substantial financial support, especially for first-time homebuyers struggling with down payments or loan repayments.

Before applying for PF withdrawal for housing, certain conditions must be met:

Your EPF account must be active

A minimum of 5 years of EPF membership is generally required

Your KYC details (Aadhaar, PAN, bank account) must be verified

The property should be in your name, your spouse’s name, or jointly owned

Meeting these conditions is essential for a smooth claim process.

The EPFO 3.0 update focuses on improving user experience and speeding up claim settlements. Key highlights include:

Fully digital claim process via UAN (Universal Account Number)

Faster processing time with minimal paperwork

Improved transparency in claim tracking

In many cases, if all documents are correct and KYC is complete, claims can be settled within a few working days.

Here’s how you can apply for PF withdrawal online:

Log in to the EPFO member portal using your UAN

Go to the “Online Services” section

Select “Claim (Form-31, 19, 10C)”

Verify your details and bank account

Choose the purpose as “Housing”

Submit the claim request

Once approved, the amount is directly credited to your registered bank account.

While using PF funds for buying a house can be helpful, it’s important to weigh the pros and cons carefully.

Your PF corpus is meant to secure your financial future after retirement. Withdrawing a large portion early can reduce your long-term savings significantly.

PF funds grow over time with interest. Early withdrawal means losing out on compounding benefits, which can affect your retirement corpus.

Before dipping into PF, consider alternatives such as home loans, savings, or government schemes. PF should ideally be used as a last resort.

Using PF funds can be beneficial in certain situations:

When you need help with the down payment

When you want to reduce your home loan burden

When interest rates on loans are high

In such cases, partial withdrawal can reduce financial stress.

Financial experts suggest that while PF withdrawal for housing is a useful option, it should be done carefully. It’s important to strike a balance between present needs and future security.

Ask yourself:

Will this withdrawal impact your retirement goals?

Can you manage without using PF funds?

Are there better financial alternatives available?

The EPFO 3.0 update has made PF withdrawals quicker and more convenient, making it easier for employees to use their savings for important milestones like buying a home. However, since PF is a long-term safety net, using it wisely is crucial.

Before making a decision, understand the rules, evaluate your financial situation, and ensure that your future remains secure while you move closer to owning your dream home.