In today’s fast-paced life, a Personal Loan often appears to be the quickest solution during financial emergencies—whether it’s for medical expenses, home repairs, or education needs. Banks and lenders promote attractive offers with low interest rates, making borrowing seem easy and affordable.

However, the reality is far more complex. The true cost of a personal loan goes beyond just the interest rate. Many borrowers overlook the fine print and later realise they are paying significantly more due to hidden charges.

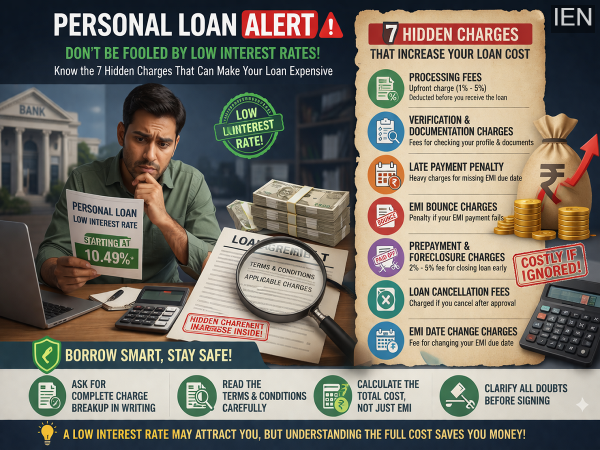

If you are planning to take a personal loan, here are seven commonly ignored charges that can quietly increase your financial burden.

Before the loan amount even reaches your account, lenders often deduct a processing fee, which can range from 1% to 5% of the loan amount.

This means:

This upfront deduction is one of the most overlooked costs.

Banks usually charge for verifying your details, including:

Though these charges may seem minor individually, they collectively add to the overall cost of borrowing.

Missing your EMI deadline—even by a day—can result in hefty penalties.

Consequences include:

Timely repayment is critical to avoid these unnecessary expenses.

If your bank account does not have sufficient balance and your EMI fails, lenders impose a bounce charge—similar to a cheque bounce penalty.

This not only increases your cost but also damages your creditworthiness if repeated.

It may sound surprising, but paying off your loan early can also come with a cost.

Banks may charge 2% to 5% of the outstanding amount as a foreclosure or prepayment fee. This is done to compensate for the interest income they lose when you close the loan early.

If you decide not to proceed after loan approval, lenders may levy a cancellation fee.

Additionally:

can also attract extra charges, which many borrowers are unaware of.

Sometimes borrowers want to align their EMI date with their salary cycle. While lenders allow this flexibility, they often charge an administrative or swap fee for changing the EMI date.

Most borrowers focus only on the interest rate while ignoring other terms and conditions. This can lead to unexpected financial stress later.

Before taking a personal loan, always:

Taking a personal loan is not a bad decision—but taking it without full knowledge can trap you in unnecessary debt.

Being informed and cautious can help you:

Remember: A low interest rate may look attractive, but understanding the complete cost of borrowing is what truly makes you financially smart.