Starting April 1, 2026, a significant change regarding your finances is set to take place—one that will directly impact your loans, credit cards, and EMIs: your CIBIL score.

Until now, the financial discipline you demonstrated—whether paying your EMIs on time or occasionally being late—has taken some time to reflect in your credit score. However, that waiting period is now over.

The RBI has implemented a new regulation: your credit score will now be updated every 7 days. The implication is clear: demonstrate good financial behavior, and you reap the benefits quickly; make a mistake, and you face immediate consequences.

First, understand these 3 key points:

From April 1st, credit scores will be updated every 7 days.

Those who pay their EMIs on time will see quick benefits, while those who default will face immediate repercussions.

Banks will now sanction loans based on real-time data, making the system significantly more stringent.

What exactly changes starting April 1st?

**Aspect** | **Current Status** | **What Changes from April 1, 2026**

**Score Update Frequency** | Every 15 days | Every 7 days

**Data Refresh Rate** | Twice a month | Five times a month

**Scheduled Dates** | Not fixed | 7th, 14th, 21st, 28th + End of the month

**Time for Impact to Reflect** | Delayed | Almost immediate

**System Speed** | Slow | Near real-time

In other words, your credit score will no longer operate in "slow motion," but rather in "fast forward."

How will the new system work? (Step-by-Step)

The RBI hasn't merely increased the speed of updates; it has completely redesigned the entire system.

1. Mandatory Monthly Full Data Submission

All banks and NBFCs:

Must compile complete data by the last day of the month;

And submit it to Credit Information Companies (CICs)—such as CIBIL or Experian—by the 3rd of the following month.

This data will include:

All your active loans;

Credit cards;

And even closed accounts.

2. Weekly Updates—But Smartly

On the 7th, 14th, 21st, and 28th of every month:

Not the full dataset, but only the changes/updates need to be submitted:

New loans/cards issued;

EMIs paid or missed;

Changes in account status;

KYC updates;

And this data must be updated within 2 days.

3. What If Banks Are Late?

The RBI's strictness will now be evident here:

CICs will file reports.

The matter will be escalated to the DAKSH portal.

Monitoring will be conducted twice a year.

In short, the game of "delayed updates" is now over.

What Changes for You?

These regulations will primarily impact the common person.

If you are disciplined:

You pay your EMIs on time.

You clear your credit card bills promptly.

The benefits:

Your credit score will improve faster.

You will get loans more quickly.

Interest rates may be lower.

If you are careless:

Late EMI payments;

Delayed credit card bill payments;

The downsides:

Your credit score could drop instantly.

Your next loan might be more expensive or get rejected.

Previously, mistakes could sometimes "slip under the radar"; now, they will surface immediately.

Benefits vs. Downsides

Your Habit | What happened before? | What will happen now?

EMIs on time | Impact was slow to appear | Score will rise instantly

Late EMIs | Could remain hidden for a while | Score will drop quickly

New Loan | Impact appeared with a delay | Will be reflected instantly

Credit Improvement | Took months | Improvement will be visible quickly

Incorrect Data | Discovered late | Opportunity for quick correction

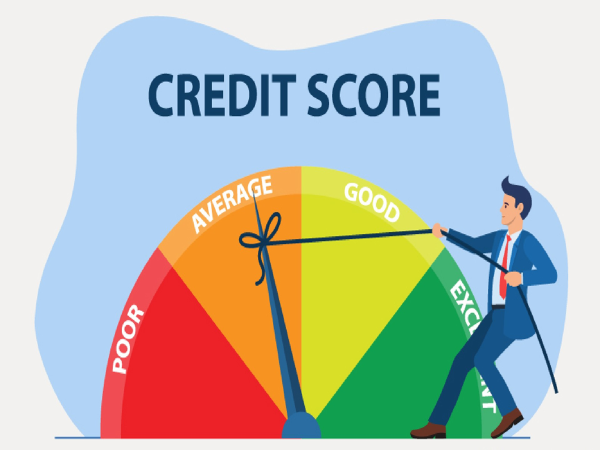

What is a Credit Score?

A credit score is a 3-digit number (ranging from 300 to 900) that indicates how trustworthy you are when it comes to repaying borrowed money.

What the Score Means:

300–550 | Poor

550–650 | Average

650–750 | Good

750–900 | Excellent

The higher your score, the cheaper your loans will be. What Changes for Banks?

Banks will now:

Look at the latest data, rather than outdated information

Make more accurate decisions

Face a reduced risk of default

In short, Obtaining a loan may not become easier, but the process will be more precise and appropriate.

What Should You Do Now?

1. Never delay your EMI payments

2. Utilize only 30–40% of your credit card limit

3. Avoid applying for loans repeatedly

4. Check your credit score 2–3 times a year

Now, Every Date Matters

Effective from April 1st, this new rule sends a clear message: the credit system has become faster, stricter, and more transparent.

From now on:

Good habits = Quick rewards

Bad habits = Immediate consequences

Therefore, every EMI payment and every specific date will now determine your financial future.

Disclaimer: This content has been sourced and edited from Zee Business. While we have made modifications for clarity and presentation, the original content belongs to its respective authors and website. We do not claim ownership of the content.