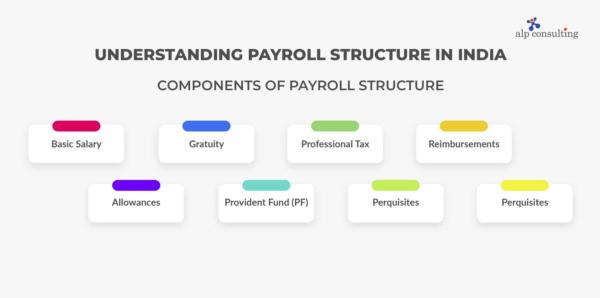

New Labour Code Update: India’s revised wage framework under the New Labour Code is set to significantly reshape how salaries are structured across industries. One of the most impactful provisions mandates that an employee’s basic pay, dearness allowance (DA), and retaining allowance must make up at least 50% of the total Cost to Company (CTC).

While this change may slightly reduce monthly take-home pay for many, it is designed to boost long-term financial security by increasing contributions toward provident fund (PF) and gratuity. However, the impact will vary depending on income level, career stage, and existing salary structure.

Under the new rules, companies can no longer allocate a large portion of salaries to allowances such as HRA, bonuses, or special perks to inflate in-hand income. If these allowances exceed 50% of total compensation, the excess amount must be shifted into the basic salary component.

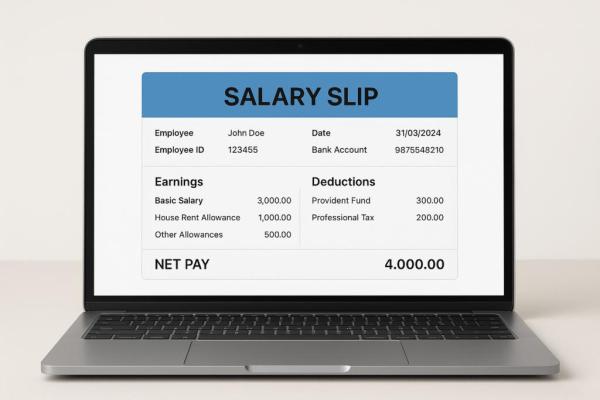

This matters because key benefits like PF and gratuity are calculated based on basic pay. As a result:

In short, employees may see a dip in monthly disposable income, but their retirement savings will grow faster.

Young employees and freshers stand to gain the most from this reform. Since they have a longer working horizon:

For those just starting out, this shift acts like a forced savings mechanism, helping them accumulate wealth without active planning.

Professionals whose basic salary previously made up less than 50% of their CTC will see the biggest structural change. With a higher base:

Though their in-hand salary may reduce slightly, the long-term payoff can be substantial.

Mid-career professionals will experience a balanced impact:

For this group, the change is less about immediate gains and more about financial discipline and stability.

6

Senior professionals and high earners are likely to feel the most immediate impact:

However, on the flip side:

So, while short-term liquidity may shrink, long-term wealth accumulation improves.

Some employees fall under the “excluded employee” category in the Employees' Provident Fund Organisation framework—typically those earning above ₹15,000 monthly and not previously enrolled in PF.

These individuals may have flexibility to:

This option allows employees to customize their savings strategy based on personal financial goals.

The primary goal behind this reform is to strengthen long-term financial security for employees. By ensuring a higher basic salary component, the government aims to:

Ultimately, the reform encourages a shift from short-term income focus to long-term financial planning.

The new wage rules may initially feel like a setback due to reduced take-home pay. However, they are designed to build a stronger financial foundation for the future.

Understanding these changes can help employees plan smarter—balancing immediate needs with long-term financial goals.

Stay informed on salary reforms, PF updates, and financial planning tips to make the most of India’s evolving employment landscape.