Planning for retirement with a target of ₹1 crore may sound reassuring today, but its real value two decades from now could be far less impressive. Financial experts consistently warn that ignoring inflation while setting long-term goals can lead to serious miscalculations. As prices rise over time, the purchasing power of money declines—making it essential to rethink how much you truly need for a comfortable retirement.

For years, ₹1 crore has been viewed in India as a benchmark for financial security after retirement. Many people assume that reaching this milestone guarantees a stress-free life. However, the reality is more complex. Inflation quietly erodes the value of money, reducing what it can buy in the future.

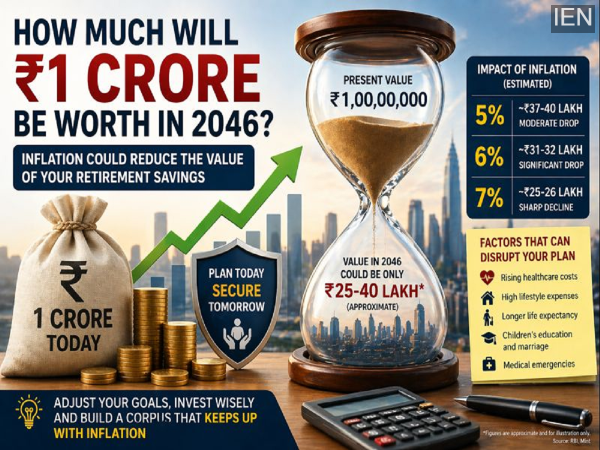

In simple terms, the lifestyle you can afford with ₹1 crore today will likely require significantly more money in 2046. Rising costs of living, healthcare, and daily essentials mean that the same amount will stretch far less over time.

The Reserve Bank of India typically aims to keep inflation within a range of 2% to 6%. Based on this range, we can estimate how much ₹1 crore today might be worth after 20 years.

Here’s a simplified projection:

These estimates highlight a crucial point—what appears to be a large retirement corpus today may not provide the same financial comfort in the future.

To understand this mathematically, inflation follows a compounding effect over time:

FV=PV(1+i)nFV = \frac{PV}{(1+i)^n}FV=(1+i)nPV

Where:

This formula shows how increasing inflation gradually reduces the real worth of your savings.

Retirement is not a short phase—it often spans 25 to 30 years or more. During this period, expenses don’t remain constant; they tend to rise steadily. Ignoring this can create a false sense of financial security.

Several key factors can disrupt your retirement planning:

Without accounting for these factors, even a seemingly large corpus like ₹1 crore may fall short.

Instead of sticking to a fixed savings target, financial planning should be dynamic. Experts suggest regularly revisiting your retirement goals and adjusting them based on inflation and changing life circumstances.

Here are a few practical approaches:

The real question is not whether you can save ₹1 crore, but whether that amount will be sufficient when you actually need it. Inflation can significantly reduce the value of your savings over time, making it crucial to plan ahead with a forward-looking approach.

A well-thought-out strategy that considers inflation, lifestyle changes, and long-term needs can help ensure that your retirement years remain financially secure—even decades down the line.