Credit card spending in India crossed ₹1.94 lakh crore in July 2025, a 12% jump from the previous year, according to the Reserve Bank of India (RBI) data. Behind that number, however, a large portion of business transactions still flows through personal cards, not out of preference, but habit.

Things like vendor bills, client travel and subscriptions all land in the same statement as personal expenses. This results in costs in clarity, credit, and convenience. A dedicated business credit card is built for exactly these challenges. Here are five clear signs that it is time to get one.

Sign 1: Personal and Business Finances Are Mixing

When you are scrolling through a statement just to figure out how to separate a client dinner and a personal grocery run, then you have a problem. Mixing personal and business finances brings accounting difficulties and makes tax filing complex.

A business owner running a proprietorship with monthly expenses of ₹2-3 lakh through a personal account, for instance, risks losing Input Tax Credit (ITC) claims worth thousands of rupees annually, simply due to a lack of documentation.

Sign 2: Cash Flow Gaps Are Disrupting Operations

The majority of businesses nowadays have phases where costs come in earlier than revenue. Having to pay for inventory, purchase invoices or marketing campaigns when awaiting client payments imposes unnecessary pressure on working capital.

A business credit card typically has an interest-free period of 30 to 55 days after the transaction date. Instead of using overdrafts and short-term loans, this float allows you to maintain your outflows as incoming payments clear.

For a business spending ₹5 lakh monthly on vendor payments, a 45-day float effectively functions as an interest-free short-term credit line, without the paperwork of a formal loan.

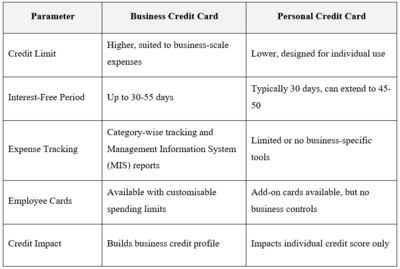

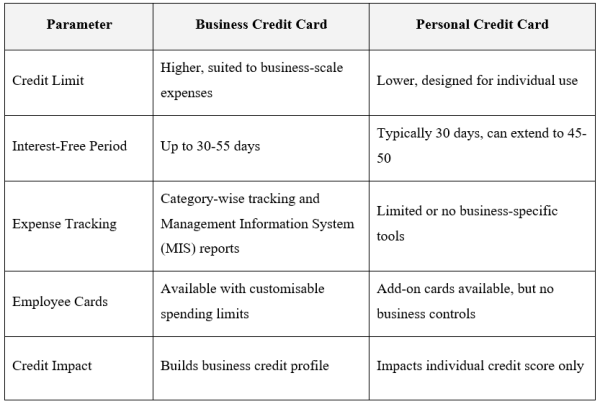

Here is how a business credit card compares to a personal credit card on key parameters:

Sign 3: Employee Expense Management Is Getting Difficult

As a team grows, so does the complexity of managing expenses. When the employees use their own money to cover their expenses and submit reimbursement claims later, finance departments waste more time examining receipts than operating the business.

For a business with even five employees in the field, reimbursement cycles typically run two to three weeks. Over a month, that can mean 15-20 individual claims, each requiring a receipt, an approval, and a manual entry.

A business credit card replaces all of that. Cards are issued with role-based limits, such as:

● ₹5,000 for field staff.

● ₹20,000 for managers.

● ₹25,000 for senior managers, etc.

Every transaction is automatically categorised, timestamped, and visible in your dashboard, saving finance teams hours.

Sign 4: The Business Has No Credit History

If you plan to apply for a loan or negotiate supplier terms in the future, lenders will evaluate your company's creditworthiness, not just your personal profile. A business with no independent credit history starts from zero every time.

Using a business credit card consistently and paying dues on time builds a credit profile under the company's name, reported to credit bureaus as a measurable indicator of financial reliability. For small and medium enterprises (SMEs) looking to scale, this foundation is worth building early.

Most Indian lenders assess the following before issuing a business credit card:

● Active business registration with valid documentation.

● A good personal Credit Information Bureau (India) Limited (CIBIL) score, especially for newer businesses.

● Income Tax (IT) returns and profit and loss statements.

● Minimum turnover or business vintage, depending on the lender.

Sign 5: Business Rewards Are Going Unclaimed

Each time you spend a personal card on a business expense, be it a flight, hotel accommodation, or a Software as a Service (SaaS) subscription, you get rewards designed for personal use. Grocery discounts and dining cashback are not much of use to a business.

Many business credit cards offer:

● Complimentary airport lounge access for frequent travel.

● Reduced foreign exchange markup fees for international transactions.

● Goods and Services Tax (GST)-compliant invoices that directly feed into your accounting workflow, reducing the manual effort of expense documentation.

Final Thoughts

Switching to a business credit card is not just a financial upgrade, but a structural move that introduces discipline and credibility in the way a business is run.

In case any of the five signs mentioned above resonates with you, it is worth evaluating whether a dedicated card fits where the business currently stands.

FAQs

1. Can a sole proprietor apply for a business credit card in India?

Yes. Sole proprietors are eligible to apply for abusiness credit card. Lenders assess personal CIBIL score and basic business documentation. Approval and credit limits vary by lender.

2. Does a business credit card affect personal credit score?

Business transactions primarily build the company's credit profile. However, as most Indian banks assess personal creditworthiness during application, responsible usage benefits both.

3. What is the standard interest-free period?

Most cards offer 30-48 days interest-free from the transaction date, with some extending up to 50-55 days depending on the billing cycle.