Five years ago, Nykaa was seen as India’s premium beauty retailer. Today, it wants investors to believe it’s building something much bigger.

At its recent Investor Day, founder Falguni Nayar looked back at Nykaa’s journey from an online beauty retailer to a broader beauty and lifestyle platform. However, her focus was firmly on the future. By FY30, Nykaa wants to cross $5 Bn in gross merchandise value (GMV), grow revenue by 2.5-3X, expand EBITDA by 4-5X, and deliver a return on capital employed (ROCE) of over 40%.

While the last decade was about building the platform, the next five years will be about extracting operating leverage. To achieve this, management believes multiple growth engines will work in tandem.

Beauty, which is already its profit driver, would continue to benefit from premiumisation. Fashion, after years of investment, is expected to move closer to profitability. Owned brands such as Dot & Key, Kay Beauty and Nykaa Cosmetics are expected to contribute a larger share of revenue and margins. Meanwhile, advertising, omnichannel retail and AI-led personalisation are likely to provide additional operating leverage.

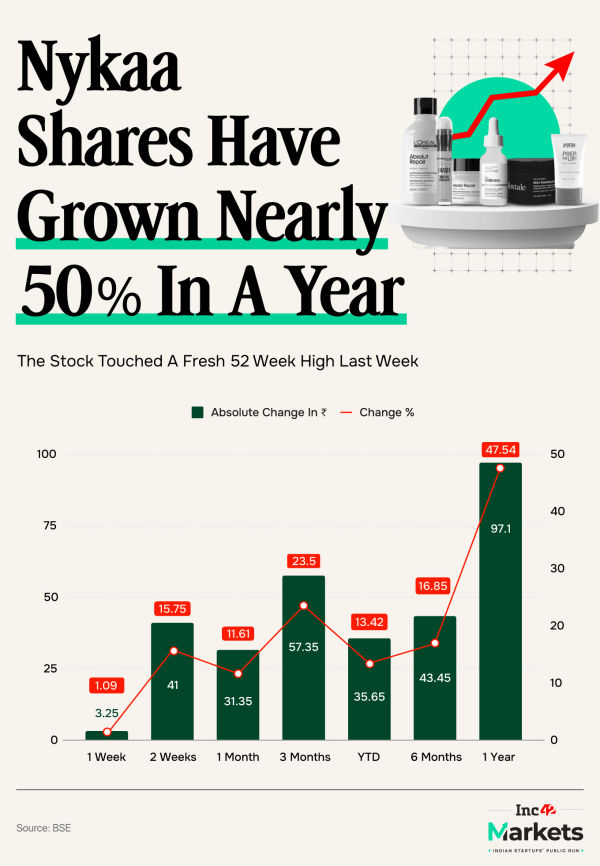

The optimism seems to be resonating well with investors. Consequently, Nykaa’s stock recently touched a fresh 52-week high of ₹309.7.

While the picture looks all rosy for Nykaa, growing revenue threefold isn’t going to be a walk in the park for the beauty major. At the same time, growing profits 5X feels overly ambitious, especially when Nykaa Fashion still does not have a market share of even 5%, as per industry estimates. This makes us question: can the beauty major live up to its own hype?

Fashion Needs To Live Up To Nykaa’s ExpectationsIf beauty is the reason investors have owned Nykaa, could fashion determine whether they continue to own it over the next five years? It is perhaps the most debated part of Nykaa’s business.

For years, fashion has been viewed as a business that required continuous investments but contributed little to profitability. While beauty steadily generated cash, fashion largely consumed it. Every quarterly result came with the same question: when would fashion finally begin delivering operating leverage?

Management now believes that the inflexion point has arrived. After nearly six years of investment, fashion is growing at roughly 40%, customer cohorts are becoming more mature, and the focus is gradually shifting from simply acquiring users to improving unit economics.

Management expects fashion’s net sales value to grow more than 3X over the next five years, while eventually delivering high single-digit EBITDA margins. If that happens, it could fundamentally change how investors value the business.

To meet management’s FY30 aspirations, fashion would likely need to compound at roughly 30-35% annually for the next several years.

Notably, fashion has humbled almost every ecommerce company that has tried to build it. Unlike beauty, fashion shopping is inherently less predictable. Consumers browse more, compare prices across multiple platforms and are far less loyal. Also, trends change rapidly, inventory becomes obsolete quickly, and return rates remain structurally higher than almost any other ecommerce category. Such realities make fashion economics considerably tougher.

Therefore, the company is also consciously moving away from being a mass-market fashion destination. Instead, it wants to own the premium segment, much like it did in beauty. Premium fashion customers generally have higher average order values, lower return rates and stronger brand affinity. Combined, these elements improve profitability over time.

Nykaa Wants To Build India’s L’Oréal“We are building a future L’Oréal or Estée Lauder out of India,” said founder and CEO Falguni Nayar. The statement summed up how management increasingly views Nykaa’s future.

Over the past few years, Nykaa has assembled a growing portfolio that includes Dot & Key, Kay Beauty, Nykaa Cosmetics, RSVP and Twenty Dresses. Management now expects these owned brands to generate more than ₹5,000 Cr in NSV by FY30, up from roughly ₹1,700 Cr today.

Investors generally like this strategy because the economics are far superior to a marketplace model. Selling third-party brands limits margins and pricing power. Owning brands, on the other hand, improves gross margins, builds intellectual property and creates long-term brand equity. That’s also why global beauty companies like L’Oréal and Estée Lauder consistently command premium valuations.

Nykaa believes it has several advantages to replicate that playbook. It has millions of customers generating valuable purchase data, one of India’s largest premium beauty distribution platforms and an expanding offline presence that helps consumers discover its brands. Dot & Key has become the company’s biggest success story so far, growing rapidly through product innovation, influencer-led marketing and wider offline distribution. Management believes this formula can be repeated across more brands, categories and even international markets.

Analysts, however, are cautious.

Much of the recent growth has come from a smaller base and acquisitions, making it easier to deliver 50-60% growth. As the business scales beyond ₹1,000 Cr, maintaining that pace naturally becomes harder. Consumer brands eventually face slower category growth, higher marketing costs and increasing competition.

The Real Question For InvestorsNykaa’s recent rally suggests investors are increasingly buying into management’s FY30 vision. Beauty still has significant room to grow, fashion appears closer to an inflexion point, and owned brands are steadily becoming a larger profit driver.

The challenge, however, is that the current valuation assumes several things go right at the same time. Beauty must continue premiumising, fashion needs to deliver on profitability, House of Nykaa has to sustain strong growth, and customer acquisition must remain efficient even as competition intensifies.

Growth does not look easy. Myntra continues to dominate online fashion, while Ajio has steadily expanded its premium portfolio. Meanwhile, Amazon and Flipkart remain formidable competitors, and new-age brands such as NEWME are becoming increasingly relevant among younger consumers.

Against this backdrop, the real question isn’t whether Nykaa can grow but whether the company can execute well enough to justify the expectations already built into the stock.

MARKETS WATCH: NEW ISSUES, POST-IPO JOURNEY & MORE

Zypp Electric’s $200 Mn IPO: Zypp Electric is gearing up for a public market debut and is looking to raise up to $200 Mn (about ₹1,890 Cr) via its IPO within the next 18-24 months. The startup has roped in Axis Capital, SBI Capital Markets and DAM Capital to manage the proposed offering.

MobiKwik Xtra Fallout: Following the MobiKwik Xtra controversy, renewed scrutiny of Per Annum and Lendbox has raised concerns over high-return investment claims, regulatory compliance, and whether P2P lending risks are resurfacing through new investment products.

Honasa’s Acquisition Spree: The Mamaearth parent will acquire a 58% stake in nutraceuticals firm Fluence Pharma for ₹135 Cr, marking its entry into the nutrition and supplements market, with plans to acquire the remaining stake over the next 5-7 years.

Meesho’s ₹202 Cr Question: Meesho’s ₹202 Cr acquisition of Kirana Club signals a contrarian bet that India’s next ecommerce opportunity lies in digitising underserved kirana retailers rather than chasing quick commerce growth.

[Edited by Shishir Parasher]

The post Can Nykaa Live Up To Its Own Hype? appeared first on Inc42 Media.