Private equity (PE) in India has undergone a transformation in the past two decades, evolving from a fledgling sector into a critical growth engine driving business expansion. In 2024, PE investments in the country to $30.89 Bn across 1,022 deals, marking a 22.7% rise in deal value and an 18.4% jump in deal count from the previous year.

Launched in 2007 by former Citigroup India directors Sumeet Narang and Gautam Gode, Samara Capital has been at the forefront of this evolution. With a sharp focus on growth sectors ranging from consumer goods to healthcare, financial services and business services/technology, this mid-market buyout PE firm has played a key role in identifying high-growth companies and scaling them for long-term success.

It acquires controlling stakes and works closely with management teams to accelerate growth and value creation. This approach, anchored in rigorous corporate governance and hands-on collaboration, has yielded significant returns. Samara has invested nearly $2 Bn across 29 companies using a blend of fund capital and co-investments and made 19 successful exits.

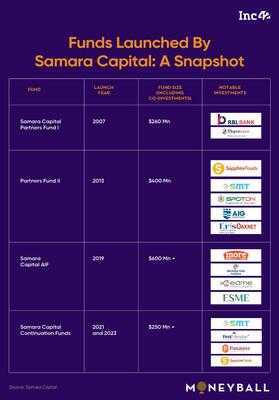

Samara has raised capital via two flagship funds and other investment vehicles that underscore the strong commitments of limited partners (LPs). Although the PE firm declined to comment on its fundraising activities, it will reportedly close its third fund in the next three to four months further fuelling its expansion in a rapidly growing PE market.

Vikram Agarwal, managing director and chief financial officer of Samara Capital, has helped script the firm’s growth story since joining in 2007. A graduate of Shri Ram College of Commerce and a chartered accountant, he had spent eight years at PwC, honing his expertise in mergers and acquisitions.

His entry into Samara was not a calculated career move. In early 2007, when the business was taking shape, its founders were searching for a chief financial officer and began reaching out through industry connections. Agarwal learnt about the opening through a chain of introductions, with one contact leading to another until the role landed on his radar. Sensing the potential, he sent his résumé, and Narang called him within an hour. The speed of response left him awestruck.

“Typically, when you send a résumé, you don’t hear back for days. Here, I got a call within an hour. That gave me an early glimpse into how this world operates — decision-making must be fast, precise and efficient,” recalled Agarwal. The initial interaction set the stage for his transition into private equity, and he took the leap.

“While at PwC, I focussed on transactions and was part of inbound and outbound M&As in India. I thought that gaining experience on the buy-side would broaden my exposure in this space,” he recalled.

Seventeen years later, his role has evolved well beyond its original scope. He initially focussed on fund accounting, investor reporting and compliance but now spends much of his time structuring and executing deals, negotiating term sheets, overseeing financing and IPO preparations of portfolio firms, and managing their litigation risks.

As Samara Capital is a buyout fund, Agarwal plays a critical role in post-acquisition financial strategy and governance, ensuring smooth transitions and operational improvements.

“What started as a finance-centric role has expanded into a broader leadership position, integrating strategy, risk management and execution across our investments,” he told Inc42 in a recent interaction as part of our Moneyball series.

According to him, Samara has maintained a flawless track record since 2012, with no losses incurred by its portfolio companies. Along the way, the PE firm has honed its expertise in handling complex transactions — mostly roll-up acquisitions that drive industry consolidation.

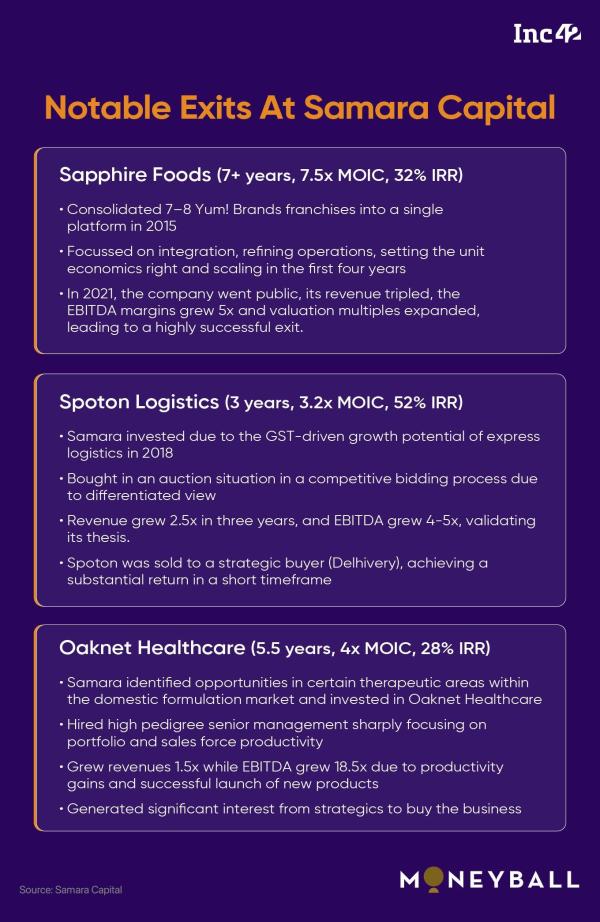

It has completed eight major roll-ups, including Sapphire Foods, where the investor merged eight Yum! Brands franchises into a leading food services powerhouse. Before this deal in 2016, these businesses ran KFC, Pizza Hut and Taco Bell outlets across India, Sri Lanka and the Maldives. Samara, in partnership with Goldman Sachs, CX Partners, and other investors, consolidated them under Sapphire Foods India, creating one of the largest regional operators of Yum! Brands.

Other notable roll-ups include FirstMeridian (human resource), ASG Eye Hospitals (healthcare) and Agam (insurance broking), each transforming smaller, fragmented businesses into scalable enterprises. In 2018, Samara collaborated with Xponentia Fund Partners to acquire Spoton Logistics for INR 550 Cr, further diversifying its investment portfolio. A year later, it invested in personal care brands such as Blue Heaven Cosmetics and Nature’s Essence. More recently, Samara expanded into packaged foods by acquiring brands like Goodricke and Continental Coffee (2023).

Beyond roll-ups, Samara Capital has set up joint ventures with leading global players. It partnered with Iron Mountain, an NYSE-listed document storage giant, and collaborated with Yum! Brands through its investment in Sapphire Foods. The firm entered grocery retail through a 51:49 joint venture with Amazon and acquired More Retail, an Indian supermarket chain. Its foray into packaged foods was further solidified through a partnership with Italy’s Colavita.

“We don’t just provide capital; we work closely with entrepreneurs to build enduring businesses,” said Agarwal, underscoring Samara’s hands-on approach to value creation. “Our ability to navigate complexity and drive strategic growth has made us the partner of choice for many companies.”

When Samara Capital started operations in 2007, India’s buyout ecosystem was still in its infancy. Therefore, for the first four years (2007-2011), the PE firm acquired minority stakes, investing in approximately 10 companies across six sectors: Consumer goods (including retail), healthcare, financial services, technology, infrastructure and agriculture & allied services.

Nevertheless, Samara’s involvement was far more hands-on, unlike traditional private equity players that primarily influence companies at the board level or through M&A decisions. It actively worked with entrepreneurs to enhance operational efficiencies, implement robust systems and processes and support strategic expansion.

This approach extended to various aspects of business development. Samara assisted portfolio companies with enterprise resource planning, enabled global expansion by identifying joint venture partners in target markets and helped secure financing for growth initiatives. Such experiences were instrumental in building the firm’s capability to manage and scale businesses effectively.

The early years were not without its challenges, though. Agarwal admitted the firm’s missteps during this period.

“The year 2007 is often cited as one of the most challenging vintages in India’s private equity landscape. Valuations had peaked, with more than 100 funds aggressively deploying capital. Yet, the global financial crisis claimed nearly 70% of those funds. We, too, were swept up in the prevailing optimism, and some of our initial investments underperformed.”

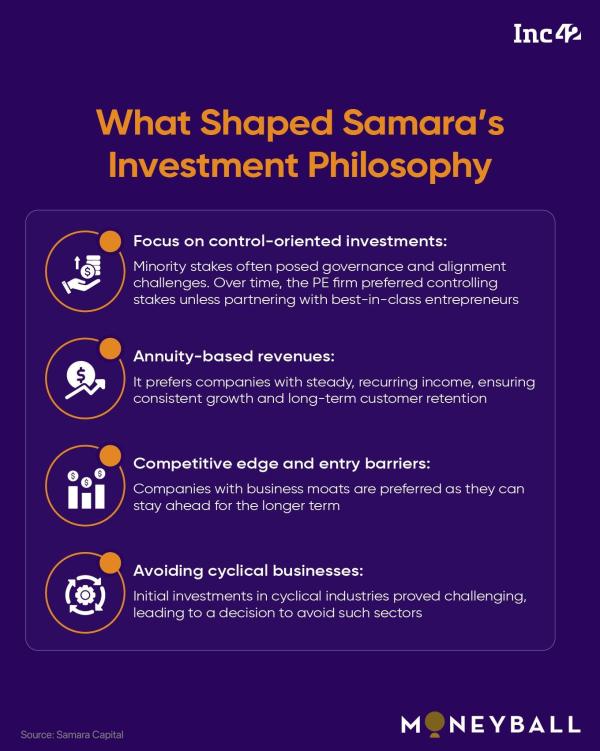

Samara carefully documented what it had learnt and built its investment strategies to avoid past mistakes. By 2012, it had moved away from agriculture and infrastructure space and focussed only on buyout deals across four verticals. It adopted a more disciplined approach and maintained rigorous pricing standards. While its early stage investments did not always reflect it, post-2012, Samara opted for a more methodical, value-driven approach to asset pricing.

Why Buyout/Control Deals Work For SamaraMore importantly, the PE made a deliberate choice to prioritise research over market trends. As Agarwal put it, “When the industry rushes toward D2C [direct-to-consumer] or high-growth models, we don’t simply follow the crowd. We conduct thorough research and only move forward if the investment aligns with our analysis.”

As Samara Capital shifted to buyouts, it concentrated on four core sectors: Consumer, healthcare, digital/technology, and financial services. Its investment thesis thrives on the owner-operator mindset, creating value for its portfolio companies.

“Buyouts offer full control over assets, enabling PEs to execute their strategic vision without external constraints. But when you hold minority stakes and collaborate with existing promoters, it often hampers your flexibility and impacts your decision-making,” said Agarwal.

“Our returns stem from two main factors — the comprehensive research we do that guides our entry at the right valuation and the value we generate post-acquisition. This ‘buy right, build right’ strategy aligns more with buyout or control deals than minority stakes,” he explained.

While ‘buy right’ ensures that investments are based on proprietary research and disciplined pricing, steering away from auction-driven valuations, ‘build right’ follows a three-pillar approach — assembling top-tier management teams, using technology to solve business complexities and implementing strong corporate governance frameworks.

Besides, the buyout ecosystem in India has seen significant growth over the past decade, making it an opportune time to explore the market for optimal outcomes. When quizzed about the growth drivers, Agarwal pointed to a couple of fundamental prerequisites.

The first is a consistent deal flow. There must be a steady stream of mid-market businesses available for sale. Historically, most Indian firms were family-owned and not actively looking to sell. The traditional mindset demanded that a company stay in the family for generations. But succession challenges have prompted a shift in perspective. Many families are now open to selling control to PE investors (instead of business rivals), as the next generation shows little interest in managing these companies.

The second is the availability of managerial talent. A well-functioning buyout ecosystem requires experienced professionals capable of running operations independently. Earlier, it was challenging to find senior executives willing to leave their corporate roles for PE-backed businesses. But this mindset has changed since 2014, especially in the mid-market segment. More professionals are now willing to transition from stable corporate careers to leadership roles in portfolio companies.

The third growth driver is leveraged finance. In the past, the country lacked a well-established lending market that would allow PE firms to secure debts for acquisitions. Today, enhanced access to leverage allows PEs to structure deals more efficiently, enabling financial closures even in capital-intensive transactions.

“Globally, buyouts account for more than 50% of private equity investments. Although this figure remains lower in India, it has grown significantly in the past decade and is expected to play an increasingly critical role in shaping the nation’s private equity landscape,” said Agarwal.

Data from EY’s Private Equity and Venture Capital Trendbook 2025 also underscores the . For instance, the dollar value of PE/VC buyout investments saw a 39% surge in 2024 to reach $16.8 Bn, a jump from $12 Bn in 2023. Interestingly, buyouts topped the leaderboard of all deal strategies, rising from the second spot in 2023 and outpacing growth investments, which saw a 21% decline in value at $13.4 Bn in 2024. Growth investments totalled $17 Bn in 2023.

The momentum continues in 2025, with buyout deals valued at $3,459 Mn in January, compared to $2,248 in December 2024 and $3,435 in January 2024.

In the startup ecosystem, early stage investments are typically backed by venture capital players, while private equity spans multiple segments, including growth stage funding, minority stake acquisitions and buyouts.

Since its inception, Samara Capital has focussed on growth stage companies, with its buyouts rooted in deep sectoral research, meticulous analysis and rigorous due diligence. The investor systematically analyses industries and identifies high-potential businesses by evaluating sub-segments for scalability, profitability and structural advantages.

“For instance, when we analysed the food sector, we noticed a great divide. Global giants like McDonald’s, Starbucks and Subway, each with a market cap exceeding $30 Bn, were in sharp contrast to smaller brands struggling to scale beyond $1 Bn. This disparity prompted us to examine the industry’s fundamental drivers of profitable growth,” said Agarwal.

After a thorough analysis, the team identified three success factors: A limited menu to reduce operational complexity, chef-independent recipes to enable scale and consistency and a focus on the food that travels well to support dine-in and delivery.

Biryani emerged as a compelling category when we tested these criteria. It is a staple dish but difficult to prepare at home; it is well-suited for delivery, and preparing it is scalable with the right processes. This insight led to Samara’s investment in Paradise Biryani.

The PE exited Paradise Food Court (the company behind the biryani chain) in 2022, selling its stake to a consortium of investors led by TR Capital in a $150 Mn secondary deal.

“We found similar attributes in pizza, chicken, and burgers, which guided our investment in Sapphire Foods,” added Agarwal.

During its research, Samara connected with Meher Chandy, then CEO of Yum! Brands India, and came to know that one of its franchises was up for sale. However, acquiring a single franchise with 60–70 outlets lacked the scale required for a meaningful investment.

“We proposed a bigger opportunity that would consolidate multiple Yum! Franchises into a single entity. We approached the other seven franchise owners, convinced them to sell, and successfully created Sapphire Foods within four to five months, starting with 250 restaurants,” said Agarwal. “We then brought in a professional management team to drive growth. Today, it is a publicly listed company, with Samara Capital as the promoter.”

Like its investment strategies, Samara follows a disciplined and structured approach for exits, balancing portfolio diversification, return multiples (multiple on invested capital or MOIC) and internal rate of return (IRR). Exits are carefully timed to maximise value creation while maintaining an optimal investment cycle.

Here is a quick look at key exit criteria:

When asked about India’s evolving private equity landscape, Agarwal outlined the importance of buyout deals, industry consolidation in a maturing market, and Samara’s selective approach towards sectors and investments.

Although it does not target typical tech startups, the PE actively explores opportunities within SaaS (software as a service), which promises more stable and predictable returns than high-risk consumer tech ventures.

While companies like Zomato and Paytm have yielded impressive returns for certain investors, Samara’s investment strategy aligns more with well-established, service-oriented tech businesses, spanning SaaS and IT services, tech-enabled business solutions, logistics, financial services and healthtech.

Regarding market volatility, Agarwal acknowledged the impact of unpredictable events like financial downturns or the Covid-19 pandemic, which can significantly stretch exit timelines. In such cases, Samara adopts a methodical approach, optimising operational costs, assessing internal liquidity, and securing external funds when needed.

With global investors accounting for just 20% of its LP base, Samara remains firmly anchored in India, concentrating on sectors where operational improvements and strategic buyouts can drive long-term value.

Although regulatory hurdles have considerably eased in industries such as insurance and pharmaceuticals, complexities persist in deal structuring due to lingering valuation norms and tax regulations, particularly for foreign investors.

Agarwal is hopeful, though. For instance, the government recently 100% FDI (foreign direct investment) for the insurance sector from the earlier 74%, opening the door for more foreign capital to boost sectoral growth. He anticipates a surge in private equity investments in India by 2030, driven by continued economic growth, greater industry formalisation and the rise of alternative funding.

As a PwC survey suggests, the next investment cycle will represent a more in India. Over the next 10 years, deals will increasingly resemble those in some developed markets. And it may be no surprise if the country sees more than $40 Bn of PE investments in 2025.

[Edited By Sanghamitra Mandal]

The post appeared first on .