Keeping large amounts of cash, gold, or investments without properly reporting them in Income Tax Returns (ITR) could create serious financial and legal problems for taxpayers in India. The Income Tax Department has intensified scrutiny of undisclosed income, unexplained investments, and unaccounted assets in recent years, and individuals failing to provide valid proof of income sources may face extremely heavy taxation and penalties.

Under current tax provisions, undisclosed income can attract tax liabilities of nearly 78 percent, while failure to explain the source of such assets may push the total tax and penalty burden close to 86 percent of the total amount. Tax experts say that understanding these rules has become essential for every taxpayer, investor, and salaried individual.

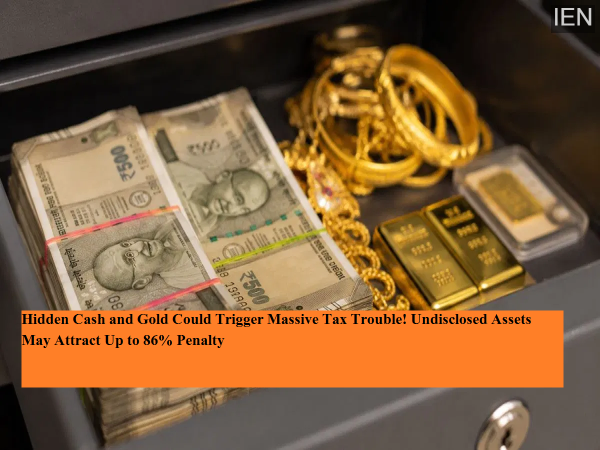

Many people keep cash savings, gold jewellery, or investments at home for personal or family security. However, if these assets are not properly disclosed in tax records or cannot be linked to legitimate income sources, the authorities may treat them as unexplained assets.

The Income Tax Department has been closely monitoring high-value transactions, benami investments, unexplained bank deposits, and suspicious financial activities. During investigations or raids, if a person fails to justify the source of money, gold, or investments, strict tax provisions under the Income Tax Act may apply.

Financial advisors warn that maintaining proper records, invoices, bank statements, and declared income details is now more important than ever.

Special taxation rules under Section 115BBE of the Income Tax Act apply in cases involving unexplained income or assets. These provisions cover matters related to:

The section becomes applicable in matters falling under Sections 68, 69, 69A, 69B, 69C, and 69D of the Income Tax Act.

Even if a taxpayer later discloses the source of such income, a very high tax rate may still apply.

If authorities detect undisclosed income and the taxpayer successfully explains its source, the amount may still attract a 60 percent base tax under Section 115BBE.

Apart from the base tax, the following additional charges may apply:

After adding these components, the total effective tax burden can rise to approximately 78 percent.

For example, if a person is found holding ₹1 crore in undisclosed income, the tax liability alone could reach nearly ₹78 lakh.

Tax professionals say many taxpayers are unaware of how quickly penalties and additional charges can escalate in such cases.

The situation becomes even more severe if a taxpayer fails to provide a satisfactory explanation regarding the source of income or assets.

In such cases, additional penalties may be imposed over and above the special tax under Section 115BBE. Combined tax and penalty charges can increase the overall recovery amount to nearly 85.8 percent.

This means that on ₹1 crore of unexplained income, the total tax and penalty burden could climb to almost ₹85.8 lakh.

Experts believe these provisions were designed to discourage tax evasion and the accumulation of black money through cash and benami transactions.

One of the most common questions among taxpayers is whether there is a legal limit on how much cash can be kept at home.

As per existing rules, there is no fixed limit on holding cash at home in India. However, the crucial requirement is that the money must come from a legitimate and explainable source.

If the Income Tax Department questions the cash holdings, the individual must be able to show:

If no supporting documents are available, the cash may be treated as undisclosed income.

Gold ownership in Indian households is common, but certain limits and conditions are also considered during tax investigations.

As per existing guidelines:

If the gold remains within these limits, authorities usually do not seize it even if purchase bills are unavailable. However, if the quantity exceeds the prescribed limits, taxpayers may need to provide proof of purchase and explain the income source used to acquire the gold.

Tax experts clarify that inherited jewellery and old family gold may also require supporting documentation in certain situations.

The government has introduced some relief measures related to Updated Income Tax Returns in Budget 2026.

Under the revised framework, taxpayers can now file an updated ITR even after receiving reassessment notices in some situations. If a person voluntarily declares previously undisclosed income and provides a valid explanation through an updated return, they may receive partial relief from harsh penalties.

However, experts note that tax deductions and exemptions are generally not available on such undisclosed income declarations.

Financial experts strongly recommend that individuals regularly review their tax filings, maintain proper documentation, and ensure that all major investments, cash holdings, and jewellery purchases are backed by legal records.

With digital surveillance, PAN-based tracking, and data-sharing systems becoming more advanced, hiding income or assets has become increasingly difficult. Taxpayers who proactively disclose income and maintain transparent records are less likely to face legal complications or financial penalties in the future.

Proper tax planning and timely ITR filing can not only prevent heavy penalties but also provide peace of mind during financial scrutiny or investigations.