Oracle Corp. reignited investor concerns about its hefty AI-related spending, triggering an 11% drop in overnight trading ahead of Thursday. However, management strongly defended the elevated investments, arguing they are essential to capitalize on a rare, hockey-stick surge in cloud demand — a case underscored by robust fourth-quarter results, and one that many retail investors appeared willing to embrace.

Oracle reported capital expenditure of $55.7 billion for fiscal year 2026, which concluded in May 2026, exceeding its own projection of $50 billion. It then said capital expenditure in fiscal 2027 would be $70 billion, and the company would spend an additional $20 billion to $25 billion for prepayments for certain components.

At the higher end, capex would exceed the company’s projected $90 billion in revenue for the year, a rarity for a Big Tech company of that size.

To achieve that, Oracle said it would raise $40 billion in debt and equity this fiscal year, including $20 billion through a previously announced program to sell shares in the open market. In the fiscal year just ended, Oracle raised $43 billion in debt financing and $5 billion in equity.

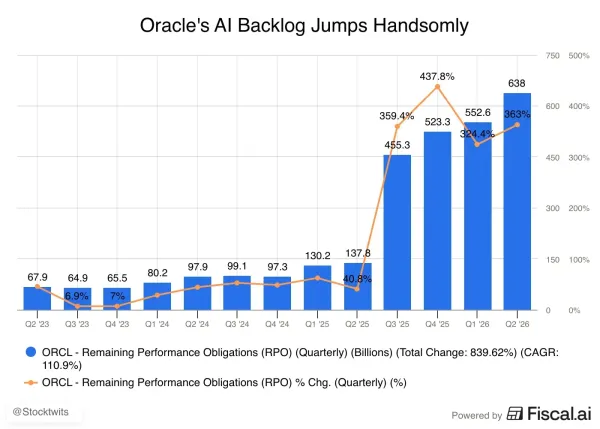

Supporting the exuberance is the incredible surge in new orders for Oracle Cloud and other services. Oracle's remaining performance obligation (RPO) — business booked but not yet realized as revenue — surged 363% year over year to $638 billion.

Oracle’s future business backlog now exceeds that of both Alphabet and Microsoft, whose RPOs, largely tied to their cloud operations, stood at $627 billion and $460 billion, respectively.

"I think that it's very important that we stay focused on customers. So the nice thing is that I think whether you see it from existing RPO or increased contracts that we're getting, yes, there's a lot of things happening in the market, but we have a large, diverse set of customers, both very large and also smaller customers,” Oracle CEO Clay Magouyrk said on a conference call with analysts.

In Q4, Oracle’s revenue surged 21% to $19.18 billion, surpassing Wall Street’s consensus estimate of $19.10 billion. Net income rose to $4.22 billion from $3.43 billion a year ago, while adjusted earnings of $2.03 per share also surpassed an expected $1.96.

Simultaneously, Oracle’s total liabilities, including debt, jumped by 48% to $218.7 billion, marking the sharpest surge on record.

“This is the kind of quarter we call mixed,” D.A. Davidson analyst Gil Luria said in an interview on CNBC. “Oracle’s remaining performance obligation is now bigger than Microsoft’s, Amazon’s and Google’s. They have more AI backlog to deliver than any of the three large hyperscalers.”

He added: “A lot of the back and forth is now around the capital raise. They’re going to need $40 billion in the fiscal year, but they stayed consistent to their previous statement that there is no more capital raise in this calendar year.”

Daniel Newman, CEO of The Futurum Group, said the results had more positives than negatives. “OCI up over 90% while backlog rips by over $80 billion. A lot to like about this as another signal of growing AI demand and lower Oracle dependence on OpenAI,” he wrote on X.

On Stocktwits, retail sentiment for ORCL shifted multiple points higher in the ‘extremely bullish’ zone (92/100), with 24-hour message volume increasing over 430%.

“$ORCL Personally, I’d give this earnings report a 9 out of 10. Revenue and EPS both beat expectations, and RPO surged to $638 billion, showing that AI-related demand remains incredibly strong,” a trader said.

“The post-earnings selloff was disappointing, but that’s also how Wall Street operates. The exact same numbers can be viewed as bullish today and bearish tomorrow, depending on the narrative the market chooses to focus on,” they said, adding that from a long-term perspective, Oracle appears to have a capital and capacity problem, not a demand problem.

Notably, Oracle shares are down roughly 20% from their recent June 1 peak heading into the earnings report. Year-to-date, shares are up 4%.

For updates and corrections, email newsroom[at]stocktwits[dot]com.<