Lululemon Athletica Inc. (LULU) has become the latest contrarian bet for famed investor Michael Burry, who believes that Wall Street may be overly focused on the athletic apparel maker’s recent stumbles while overlooking the long-term strength of its brand, balance sheet and growth potential.

In his latest Substack post, Burry said Lululemon has endured several high-profile setbacks throughout its history, and some investors believe the company is confronting another pivotal moment.

Lululemon has faced several controversies linked to founder Chip Wilson, including criticism over marketing campaigns and public comments that upset some customers.

Burry said a new tax law introduced by President Trump in his first term increased costs for Lululemon’s overseas operations, reducing the company’s gross margin by about 2.5 percentage points.

“As shares languished, LULU’s infamous CEO carousel continued to spin. A management void developed. It was as if no one is in charge. The stock fell more.”

According to Burry, after struggling for about five years and undergoing multiple leadership changes, Lululemon rebounded when CEO Calvin McDonald took office in 2018. Within a year of his arrival, profit margins recovered to record levels, and the stock surged, breaking past previous highs in 2018 and quadrupling from its 2014 low.

“Today, in fact, Lululemon is suffering under another federal order – also from President Trump, now in his improbable 2nd term. This time, Trump II’s tariffs are killing gross margins. Even though LULU was ahead of the curve getting out of China, its new locations are all tariffed too,” said Burry.

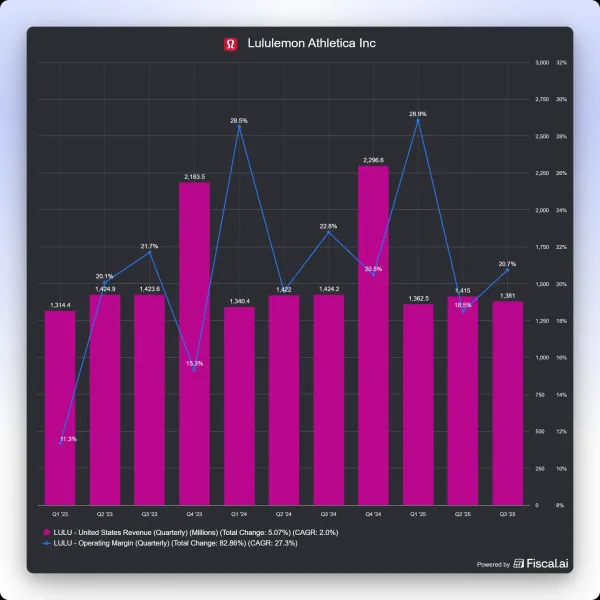

Management said tariffs alone reduced product margins by nearly three percentage points in the latest quarter.

Burry explained that Lululemon's recent troubles began in 2024 with the launch of Breezethrough leggings, which drew criticism over their design and transparency issues, forcing the company to pull the product.

The company currently lacks a permanent CEO, with a new leader arriving from Nike in September. Investor sentiment has deteriorated sharply. Burry said the stock has fallen to around $104 from more than $423 in early 2025.

While North American sales have softened, China continues to generate growth. However, even that market has not been immune to controversy, with a recent marketing event drawing criticism on Chinese social media.

Lululemon Athletica stock edged 0.08% lower overnight, ahead of Thursday. The stock is trading at a seven-year low.

Burry argues that Lululemon has become an overlooked, out-of-favor stock much like Ross Stores in 2000. He believes investors are fixated on AI-related companies and ignoring a profitable retailer whose temporary problems may create significant long-term upside.

He says the key question is whether Lululemon can remain a relevant brand for decades. Though he acknowledges growing competition from newer athleisure labels like Alo, Vuori, he believes they pose only limited threats to Lululemon.

“LULU is not losing too many people who like to sweat to ALO or Vuori, and in fact at least 95% of LULU’s customers are not customers of either of the upstarts,” said Burry.

According to Burry, Lululemon's stock has become excessively depressed due to temporary issues and overly pessimistic narratives. He believes the valuation now offers compelling upside, similar to past successful investments in beaten-down retail brands.

“Bad management is a value investor’s best friend. If not for bad management, the world would be more boring, less colorful,and less undervalued. Of course, like all best friends, bad management should not overstay its welcome,” added Burry.

Burry added that Lululemon’s enduring brand strength has repeatedly overcome management mistakes. He argues poor execution has created an opportunity, and a successful turnaround under incoming CEO Heidi O’Neill could unlock significant value.

“The business is not falling apart. It is simply not growing due to multiple mistakes, lack of management, lack of execution, and regulatory hits with tariffs and the extinction of the de minimis exemption,” he said.

Burry concluded his analysis, saying Lululemon remains financially strong, with substantial cash, minimal debt, solid returns on capital, and growing book value. He believes the stock's valuation has fallen to unusually cheap levels despite healthy fundamentals.

“LULU is the one and only U.S. clothing retailer of any market capitalization trading at less than 3x tangible book and less than 10x earnings,” said Burry.

LULU stock has cratered 45% year-to-date.

For updates and corrections, email newsroom[at]stocktwits[dot]com.<