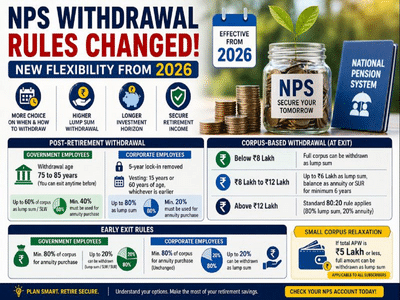

The government has introduced a major update to withdrawal rules under the National Pension System, giving subscribers greater flexibility in accessing their retirement savings. These revised norms, notified by the Pension Fund Regulatory and Development Authority (PFRDA), will come into effect from 2026 and aim to simplify exit options for both government and corporate sector employees.

Here’s a clear breakdown of how the new rules will impact withdrawals before and after retirement.

Post-Retirement Withdrawals: More Flexibility for Subscribers Government Sector EmployeesUnder the updated framework, the maximum age to stay invested in NPS has been extended from 75 to 85 years. This means subscribers can continue earning returns on their pension corpus for a longer period. However, they still retain the flexibility to exit earlier if needed.

At the time of retirement or exit:

This structure remains unchanged but now comes with extended investment duration.

Corporate Sector EmployeesThe revised rules bring significant changes for private-sector subscribers:

Most notably:

Earlier, only 60% withdrawal was permitted, making this a substantial relaxation.

Corpus-Based Withdrawal RulesThe new framework introduces withdrawal flexibility based on the size of the accumulated pension wealth (APW):

This tiered approach ensures that smaller investors have easier access to their funds.

Early Exit Rules: What Happens Before Retirement? Government EmployeesFor those opting for premature exit:

Early withdrawal rules remain largely unchanged:

A major relief applies to all subscribers:

This ensures that smaller investors are not forced into annuity purchases unnecessarily.

Why These Changes MatterThe updated NPS withdrawal rules are designed to strike a balance between liquidity and long-term financial security. By offering more flexible exit options, the government aims to make the pension system more user-friendly and aligned with diverse financial needs.

Key benefits include:

With these changes coming into force in 2026, NPS subscribers should review their retirement plans carefully. The increased flexibility offers new opportunities—but also requires smarter decision-making to ensure long-term financial stability.

Understanding when and how you can withdraw your pension savings can make a significant difference in securing a comfortable post-retirement life.