Promoter shareholding is considered a barometer of their confidence in the business. However, promoters often reduce their shareholding by selling a part of their stake.

This selling can be due to any reason un to the company’s performance, which is not always a sign of trouble.

However, in many cases, it indeed signals caution. On the same note, we have picked 2 stocks with declining shareholding. Is it a time to be cautious with them? Let’s see.

#1 Home First

Home First is one of the leading players in terms of market share in the affordable housing segment, with assets under management (AUM) of ₹97 billion (as of FY24).

The company primarily offers home loans to low to middle-income group borrowers with an average ticket size of ₹1.2 million. It operates through 133 branches across 343 touch points in 135 districts.

Home First has witnessed strong growth in AUM over the last four years, growing from ₹36 billion in FY20 to ₹97 billion in FY24, at a compound annual growth rate (CAGR) of 28%. The AUM growth was driven by strong momentum in disbursements, which grew at a 25% CAGR during the period as real estate demand boomed post-pandemic.

The company’s AUM primarily comprises secured loans, with 86% of its AUM in FY24 composed of home loans and the rest from shop loans and loans against property.

In addition, 68% of the AUM comes from salaried individuals, with the rest from self-employed individuals. This protects Home First AUM from credit quality shocks.

With a strong collection efficiency of 99%, Home First’s asset quality is also strong. Its gross non-performing assets (NPA) and net NPA are 1.7% and 1.2%, respectively – one of the best in the industry.

With strong asset quality, the company credit cost remains the lowest in the industry at 0.3% (in FY24), down from 1.8% in FY22. Strong AUM growth and low credit costs mean Home First sets aside less capital for loan losses, boosting profitability.

Home First’s net interest income grew at a 33% CAGR over the last four years, from ₹1.5 billion in FY20 to ₹4.7 billion in FY24. Meanwhile, net profit grew at a 40% CAGR to ₹3.1 billion in FY24.

With strong profit growth, the company’s return ratios have also increased steadily. Its return on average assets has risen from 2.7% in FY20 to 3.8% in FY24. On the other hand, return on equity has increased from 10.9% to 15.5% in FY24.

Home First Finance is a private equity-backed company, with True North and Aether (Mauritius) Ltd as its key promoters. Notably, like every PE fund, it has been selling shares, resulting in its aggregate shareholding falling from a high of 33.5% in Q3FY24 to 14.3% in Q3FY25.

Looking ahead, Home First aims to grow its AUM at CAGR of 27-30% in the next two years. To this end, the company hopes to add 30-40 branches next year and further strengthen its presence in existing geographies.

Its debt-to-equity ratio remains at 3.4x, with management aiming to maintain leverage at around 5x over the medium term. Further, rising interest rates put pressure on Home First spreads in FY24. As a result, the spread declined to 5.4% from 5.7% last year. Management expects the spread to remain at 5.2% over the medium term.

Home First is trading at 4x book value (FY24), in line with its 4-year average of 4.1x. Compared to peers, it is trading at a premium to Aptus Value Housing (3.7) and Aadhar Housing (3.2) but lower than Bajaj Housing (5.4).

Motilal Oswal says Home First has invested in building a franchise that positions itself well to capitalise on the significant growth opportunity in affordable housing finance. It has a buy rating on the stock, with a target of ₹1,280, an upside of about 28% from the current price.

#2 Godrej Consumer

Godrej Consumer is part of the Godrej Group of companies. In 2001, the company was formed from the demerger of the consumer productions division of erstwhile Godrej Soaps.

Godrej Consumer is a fast-moving consumer goods company with a significant presence in household insecticides, hair colours, home and car air fresheners and liquid detergents.

The company is the market leader in household insecticides, hair colour, and air freshener categories and the second largest company in the soaps category in the domestic market.

It has also acquired Raymond’s FMCG business along with the trademarks of leading brands Park Avenue, KS (deodorants), Kama Sutra and Premium for Rs 28 billion, further strengthening its position in the sector.

The company’s operations are highly diversified. India contributes 59% to its consolidated revenue, while 13% comes from Indonesia and 23% from Africa, the USA, and the Middle East. Further, Personal Care contributes 59% to Godrej Consumer’s revenue, Home Care (38%), and Others (3%).

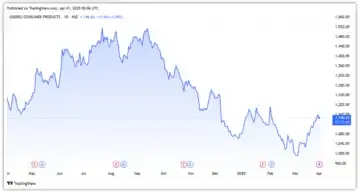

Company revenue has grown at a modest 9% CAGR during the last four years, from ₹99 billion in FY20 to ₹141 billion in FY24. However, growth has recently slowed due to a degrowth in the Indonesia and Africa segments, as seen from inventory turnover, which rose to 9.9 from 7.2 last year.

On the other hand, its net profit has grown at a modest 5.7% CAGR, from ₹15.7 billion to ₹20.4 billion in FY24. Godrej’s margins have remained relatively stable, between 19% and 22%.

The company’s India business rose 9% year-on-year in FY24 to ₹84 billion, driven by 13% volume growth. The segment margin stood at 26.7%, improving from 24.2% in FY23, as raw material costs decreased.

Prompter holding in the company fell to 53% in Q3FY25 from 63% in Q2. The decline is due to the realignment of shareholding in various Godrej Group companies following a family settlement agreement that split the 127-year-old conglomerate into two.

Despite the strong performance of the broader business, the company faces pressure on demand and margins in the near term due to a slowdown in consumption. Nevertheless, the company plans to accelerate growth in the long term through strategic initiatives.

To this end, the company plans to increase its market share in rural areas by doubling outlet coverage and tripling village coverage. It focuses on high single-digit volume growth in India and Indonesia, while profit and cash flow in other regions.

The company is also scaling up across premium channels and experiencing high single-digit growth in modern trade and e-commerce. It also aims to drive growth in Raymond Consumer’s newly acquired brands.

The company trades at a price-to-equity ratio of 68x, 36% higher than the 10-year median P/E of 49. Relatively, it is trading at a premium to Dabur (50), Emami (32), and Hindustan Unilever (50). JPMorgan has maintained its overweight call on Godrej Consumer with a target price of ₹1,410, 23% higher than CMP.

Conclusion

The promoter may sell shares for various reasons, which may or may not always be bad. For example, Home First, backed by private equity, looks to exit after a certain period to return capital to investors or pursue better opportunities. In Godrej Consumer, the sale is due to the division of the Group business.

In both cases, these are strategic decisions, and there appears to be no need for concern as long as the business fundamentals remain strong.

Disclaimer

Note: We have relied on data from throughout this article. Only in cases where the data was not available, have we used an alternate, but widely used and accepted source of information.

The purpose of this article is only to share interesting charts, data points and thought-provoking opinions. It is NOT a recommendation. If you wish to consider an investment, you are strongly advised to consult your advisor. This article is strictly for educative purposes only.

About the Author: Madhvendra has been deeply immersed in the equity markets for over seven years, combining his passion for investing with his expertise in financial writing. With a knack for simplifying complex concepts, he enjoys sharing his honest perspectives on startups, listed Indian companies, and macroeconomic trends.

A dedicated reader and storyteller, Madhvendra thrives on uncovering insights that inspire his audience to deepen their understanding of the financial world.